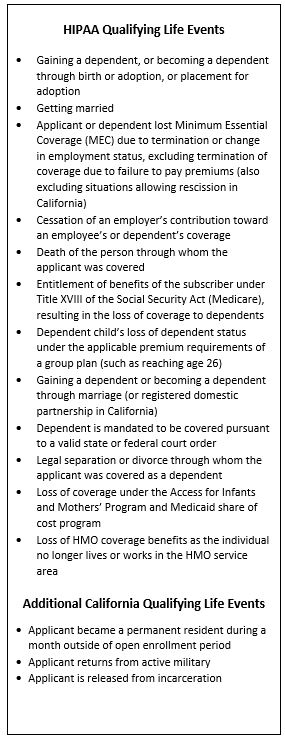

Generally, health insurance consumers cannot enroll in health coverage outside of an open enrollment period unless the consumer experiences a qualifying life event allowed under the Health Insurance Portability and Accountability Act (HIPAA).

HIPAA qualifying life events grant special enrollment rights to health insurance consumers who previously did not enroll in health coverage. States can add more designated qualifying life events, in addition to those allowed by HIPAA. Under the law, consumers are eligible to enroll in coverage outside of the plan’s annual open enrollment only within a certain timeframe.

Employer-sponsored Group Health Insurance Plans have annual open enrollment periods where employees can enroll in a health insurance plan, switch plans, and/or add or remove dependents from their coverage.

Likewise, Individual and Family Plans (IFP) have open enrollment periods (with the same allowances) both on and off state Exchanges, such as Covered California or the Nevada Health Link.

Open enrollment periods exist to combat adverse selection challenges. Without open enrollment periods, health insurance consumers might wait to enroll in coverage until they become sick – and the health insurance system would not work.

There are generally two types of special enrollments: upon loss of eligibility for other coverage, and upon certain life events.

Upon Loss of Eligibility for Other Coverage

Employees and dependents who decline coverage under an employer-sponsored plan because they have other coverage and then lose that coverage, either due to loss of eligibility or loss of employer contributions, have special enrollment rights.

For example, an employee turns down health benefits for herself and her family because the family already has coverage through her spouse’s plan. Coverage under the spouse’s plan ceases. That employee can then request enrollment in her own employer’s plan for herself and her dependents outside of open enrollment.

Upon Certain Life Events

Employees, spouses, and children are permitted to special enroll on coverage outside of open enrollment due to marriage, birth, adoption, or placement for adoption.

Timeframes

For both types of special enrollments allowed by HIPAA qualifying life events, the employee must request enrollment within 30 days of the loss of coverage or life event that triggered the special enrollment. An exception to this rule is when employees and/or their dependents lose coverage under a state Children’s Health Insurance Program (CHIP) or Medicaid. The employee or dependent, in this case, must request enrollment within 60 days of the loss of coverage.

Available Assistance

If you have any questions concerning HIPAA or state qualifying life events, your WBCompliance team is as near as your telephone or email. Call 866-375-2039, or email compliancesupport@wordandbrown.com.